**Abstract**

Core Tip: Overall, we expect copper prices to stabilize in the short term, with a low likelihood of further declines next week. However, this does not change our long-term view that copper prices are likely to remain weak. The short-term support level for copper is around $6,600, with resistance at $6,800 (more likely to be broken), and a secondary resistance at $7,000. The corresponding price range is between 4.75 million and 5 million yuan. Spot copper is currently trading between 4.8 million and 5 million, while scrap copper ranges from 4.52 million to 4.72 million.

**First, Electrolytic Copper Market**

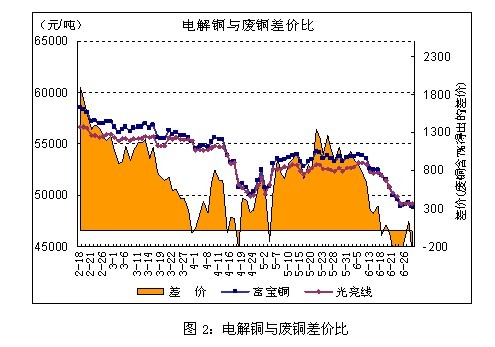

After last week’s sharp drop, copper prices remained relatively stable this week, showing a volatile but bottom-bound trend. The spot copper price has not changed significantly, with fluctuations remaining under 1,000 yuan. According to the data collected this week, the following chart illustrates the trend:

The bearish sentiment in the spot market continued this week, with bank fund shortages affecting traders’ willingness to hold inventory. At the end of the month, spot traders were eager to sell, leading to wide discounts. Unlike the futures market, where buyers and sellers often engage in transactions, spot traders tend to be more cautious. With low-cost copper available, only raw material factories requiring continuous production have been purchasing on demand, while other businesses have remained inactive. Middlemen have seen limited profit margins, and overall operations have been quiet. However, cash flow among spot holders became more apparent, especially on Friday, the last business day of the second quarter, when many banks closed their systems for quarterly settlements. As a result, copper traders paused their activities, and transactions were generally unsatisfactory. If the current cycle continues, it is expected that spot transactions will remain difficult to improve.

Another chart shows the Shanghai-London ratio, which had been rising before this week but now shows a downward trend. Import losses have also widened, making the current environment unfavorable for copper imports. Bonded area copper stocks have not dropped sharply recently, and there have been rumors of a major copper company facing financial difficulties due to a capital chain issue. This highlights the impact of recent banking problems on the copper market.

Due to the low domestic supply and the fact that bonded area inventories are locked by importers and foreign banks, the Yangshan copper premium has continued to rise, reaching around $200 per ton. Some spot traders believe this trend may continue, potentially supporting current copper prices. Additionally, this week saw a decline in spot copper discounts, with a 6.6% increase in LME copper cancellation warehouse orders. This suggests that European demand may have improved slightly. Overall, it is expected that copper prices will remain stronger than Shanghai copper next week, causing the Shanghai-London ratio to rise.

**Second, Recycled Copper Market**

1. **Electrolytic Copper and Bright Lines**

From Monday to Friday, scrap copper prices showed a slight decline followed by a flat trend. Foshan 1# bright line fell from 46,650 on Monday to 45,950 on Friday, a decrease of 700 yuan. The price of electrolytic copper was similar to that of bright line, dropping by 1,150 yuan compared to last week. Prices were weak in the first two days, but from the third to fifth days, scrap copper prices stabilized, and the market saw very little transaction activity.

Currently, the declaration of scrap copper remains challenging, and no improvement in imports has been observed. The spot market is affected by the sharp drop in copper prices, with merchants reluctant to sell and goods becoming increasingly scarce. Domestic scrap copper raw materials are insufficient, and the combination of import issues and reluctance to sell has led to tighter market supply. Although the supply shortage has provided some support to scrap copper prices, the weak copper price has weakened the advantage of scrap copper, leaving its support inadequate. Most scrap copper processing companies are either idle or operating at half capacity, and market demand has shifted toward refined copper processing. This has caused some domestic copper processing enterprises to reduce or halt production, adopting a wait-and-see approach. Some scrap metal trading markets are nearly empty, with few goods available for sale.

At present, the pressure on the domestic copper market is significant, with high inventory levels and weak demand. The future trend of copper prices is unlikely to change soon.

2. **Copper Pipe Enterprises Operating Rate in June**

According to recent investigations into the production status of copper pipe enterprises in June, the average operating rate for copper wire companies was 75.8%, up 2.3% from 74.05% in May. One company stated: “Actually, May and June production levels are almost the same. It is peak season, but July will definitely see reduced production. The peak season is over, and off-season production must be cut.†Overall, the main market is weak, with poor order levels and low procurement enthusiasm. Copper pipe enterprises have been engaged in price competition for a long time, with limited profit margins. We believe that late copper consumption will not be strong, and any turnaround will likely occur during the golden September and October seasons.

**Third, Downstream Market Analysis**

This week, the ex-factory price of Zhejiang Jinlong Hpb58-3 brass rod remained at 36,500 yuan per ton. Since the price of copper fell last week, the price of brass rods has remained largely stable. Due to the turbulent copper price movement this week, the sideways fluctuation has had little impact on pricing. Merchants are currently on the sidelines, and price adjustments are being made cautiously.

Overall, the turnover in the downstream copper market has been good. However, due to the sharp drop in copper prices and the low season, many merchants have seen a decline in orders and output. According to research data from the Fubao Copper Research Group, the average operating rate of copper pipe enterprises in June was 75.8%, which is basically the same as in May. Small and medium-sized enterprises have seen a decline in start-up rates. Merchants report that they will enter the off-season in July and August, with declining demand for household appliances such as air conditioners. In addition, due to summer temperatures, the load on general processing and smelting merchants will decrease, reducing production capacity. Currently, the falling copper price has narrowed the trade margin space for companies, and some copper companies have faced rising raw material costs. The accumulation of capital has put pressure on company funds. Overall, downstream enterprises have concentrated orders in May and June, and are now overcrowded. Large enterprises with fixed channels can still maintain stable construction in July, but SMEs, affected by terminal demand and price fluctuations, find it difficult to maintain order volumes.

Cable companies are also facing a crisis of declining orders. While large enterprises are supported by national bidding orders and can maintain high-load operations, many small and medium-sized enterprises still have an advantage in terms of proportion. According to survey data, cable companies in Anhui, Shandong, and Zhejiang have seen a slight decline in average starts in June, although infrastructure projects still have a positive effect on driving cable consumption. In the short term, the low copper price has weakened enterprise profitability, and production enthusiasm naturally declined. July is also a low season, so the decline in orders is reasonable.

**Fourth, Futures Market Analysis and Forecast**

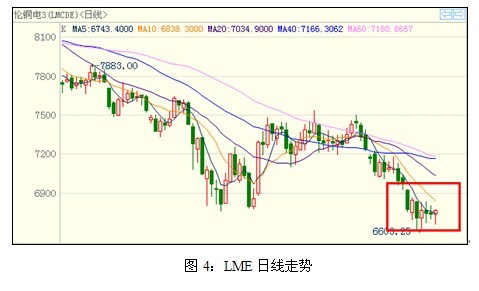

This week, copper prices fell to the level of $6,600, recording a new three-year low, then rebounded slightly, stabilizing after the decline. The following chart shows the trend:

This week, global macroeconomic focus has been on China. At the beginning of the week, interbank financial tensions spread to the market, causing a sharp drop in commodity and stock markets. The Shanghai Composite Index fell to “pre-liberation†levels; however, with the State Council's signal of maintaining stability and repeated emphasis on market fundamentals, the higher interbank lending rate has returned to a more stable state. From the central bank's attitude, it is clear that the government is determined to adjust the economic structure. Financial de-leveraging is urgent, and the central bank is changing its previous image of "nother." Additionally, urbanization is gradually showing "spikes," with over 300 billion yuan allocated for slum renovation injecting new impetus into economic growth. It is difficult for the country to tolerate economic growth below 7.5%, and the government's ability to control the economy remains strong.

In Europe, economic data show that the Eurozone economy is gradually improving, particularly in Germany, the locomotive of the region. However, the impact of the debt crisis still exists, and Italy will face more challenges in the future. In the United States, with Bernanke's statements dominating the market, the dollar has surged, government bond yields have risen sharply, and market panic persists. As the Fed’s explanation of monetary policy gradually eased market concerns this week, the exit from quantitative easing is related to economic growth, and there will be no exact date for withdrawal.

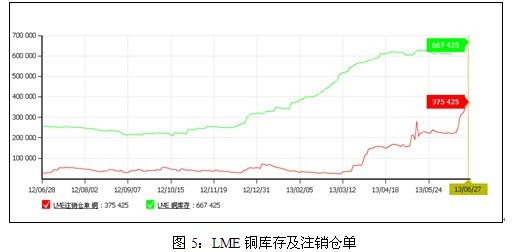

Fundamentally, this week focused on LME copper stocks and canceled warehouse receipts. As shown below:

From a trend perspective, both copper stocks and canceled warehouse receipts have fluctuated and increased. Inventories rose to a maximum of 670,000 tons, then slightly decreased. However, it is important to note that the percentage of canceled warehouse receipts reached 55.63%, exceeding 370,000 tons. The rise in canceled warehouse receipts will ease the pressure of high copper stocks, help alleviate the bearish atmosphere, and support copper price stabilization.

According to data from the International Copper Study Group (ICSG), the global refined copper market had a surplus of 104,000 tons in March 2013. In March, global copper production was 1.804 million tons, and consumption was 1.7 million tons. ICSG said that in the first quarter, the global refined copper market had a surplus of 222,000 tons, compared to a deficit of 312,000 tons in the same period of 2012. Data show that in the first three months of 2013, global copper use was 4.966 million tons, a 5.3% decrease from the first quarter of 2012. In China, copper consumption decreased by 10%, and net imports of refined copper decreased by 46%. China is the world's largest consumer of copper, accounting for about 40% of global demand.

Investment banks' latest forecasts: Morgan Stanley expects copper prices in 2013 to be $7,800 per ton; the 2014 average price forecast is $7,900 per ton. Credit Suisse lowered its 2013 average copper price forecast from $7,482 per ton to $7,240, and its 2014 estimate fell from $6,675 to $6,225. Goldman Sachs announced a new copper price estimate, expecting copper prices to be $7,000, $6,600, and $6,600 per ton for three, six, and 12 months respectively, compared to $7,500 and $8,000, and $7,000.

From a technical standpoint, copper prices are in a long-term decline, and lower prices are expected in the second half of the year. In the short term, copper has strong support between $6,500 and $6,600, with the KDJ indicator having bottomed out. There are signs that the possibility of a short-term downtrend is increasing, and next week’s copper price trend will depend more on China’s economic data.

In summary, we are more inclined to expect copper prices to stabilize in the short term, with a low likelihood of further declines next week. However, this does not change our long-term view that copper prices will remain weak. Short-term support for copper is at $6,600, with resistance at $6,800 (more likely to be broken), and a secondary resistance at $7,000. The corresponding copper price range is between 4.75 million and 5 million. Spot copper is currently trading between 4.8 million and 5 million, while scrap copper ranges from 4.52 million to 4.72 million.

Â

Kitchen sink

The main purpose of the kitchen sink is to wash food, wash dishes, etc. According to the style, it can be divided into Apron Sink, workstation, Topmount Sink, Undermount Sink and so on. The sink is mainly made of 304 stainless steel, which is resistant to corrosion, oxidation, good toughness and durability.

Â

Over 10 years global trade of stainless steel handmade kitchen sinks experience.

High quality 304 or 201 stainless steel material, apply advanced nano technology.

Customized different sizes and colours to satisfy different demands.

Kitchen Sinks,Double Bowl Sink,Farmhouse Sink,Handmade Stainless Steel Sink,Stainless Steel Sink

Jiangmen MEIAO Kitchen And Bathroom Co., Ltd. , https://www.meiaosink.com